YEAR 2024-2025

On the 30th of June 2025, the JPC held an Extraordinary meeting to consider and approve the Annual Governance and Accountability Return.

Copies of the AGAR documents are listed below. Residents should be aware of the Notice of Public Rights posted herein today, 30 June, and extending until 9 August.

Accounting Statements – Section 2

Explanation-of-Variances-Proforma

Reconciliation-between-Box-7-and-Box-8-Proforma

Notice-of-Conclusion-of-Audit-24_25

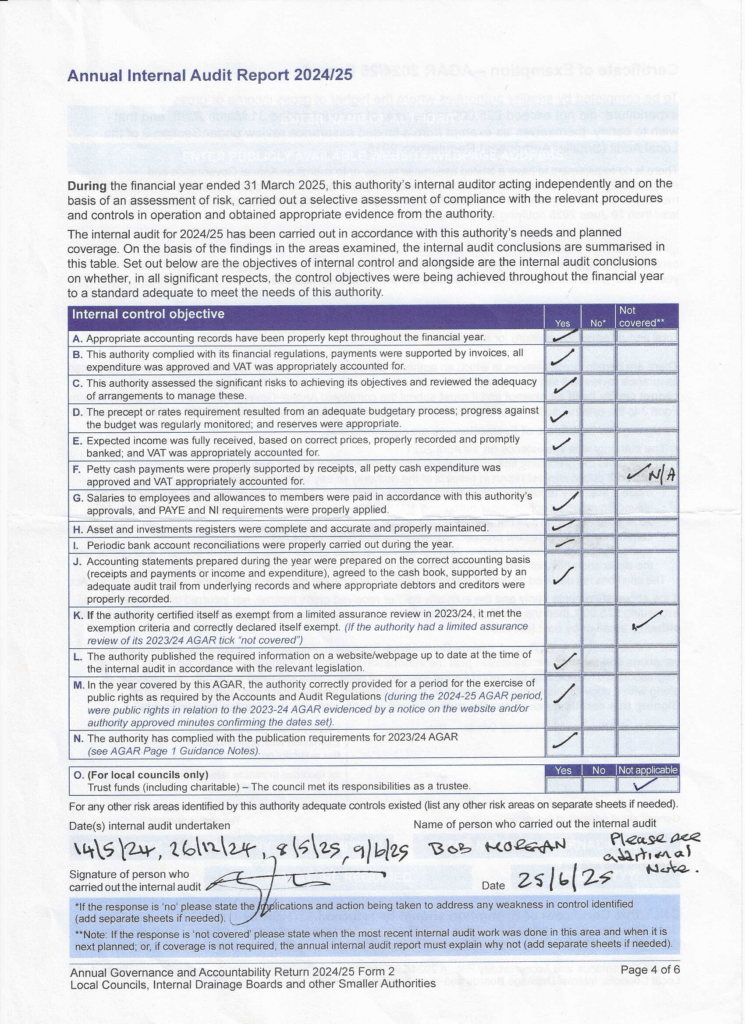

Notice of Conclusion of Audit 2024/25

Beaudesert & Henley-in-Arden Joint Parish Council has received the signed External Auditor Report and Certificate for the financial year 2024/25.

In accordance with the Accounts and Audit Regulations 2015, the Notice of Conclusion of Audit has now been published, along with Sections 1 and 2 of the Annual Governance and Accountability Return (AGAR).

These documents are available to view on this website and may be inspected by any local elector. The audit confirms that the Council’s accounts have been reviewed and certified by the external auditor.

Signed EA Certificate 2025 – Beaudesert and Henley in Arden Joint Parish Council_1873256

YEAR 2023-2024

The JPC have successfully concluded the 2023-2024 return without need for further engagment. The relevant closure doccuments are listed below, please take a moment to look through all of the items displayed:

CONCLUSION OF AGAR LETTER 23-24

SECTION 3 – EXTERNAL AUDITORS REPORT 23-24

SIGNED NOTICE OF CONCLUSION 2023-2024

On the 3rd of June 2024, the JPC held a public meeting which under Item 11 of the Agenda, including a full membership appraisal of the Annual Return.

The matter of the Annual Governance & Accountability Return was considered and approved by full Council.

Copies of the completed documents are listed in the following, residents should be aware of the Notice of Public Rights posted herein today, and extending until the 15th of July 2024.

SECTION 2 REV. 2 ASSETS TYPO AMENDED 29.07.2024

SECTION 2 REV. 1 BORROWINGS ADDED 23.06.2024

COMPLETED SECTION 1 – ANNUAL GOVERNANCE STATEMENT [1 page]

COMPLETED SECTION 2 – ANNUAL ACCOUNTING STATEMENT [1 page]

EXPLANATION OF VARIANCIES PROFORMA [1 page]

NOTICE OF PUBLIC RIGHTS [1 page]

RECONCILIATION BETWEEN BOX 7 AND BOX 8 PROFORMA [1 page]

Further information on this process as it occurs will be posted on this page over the coming months.

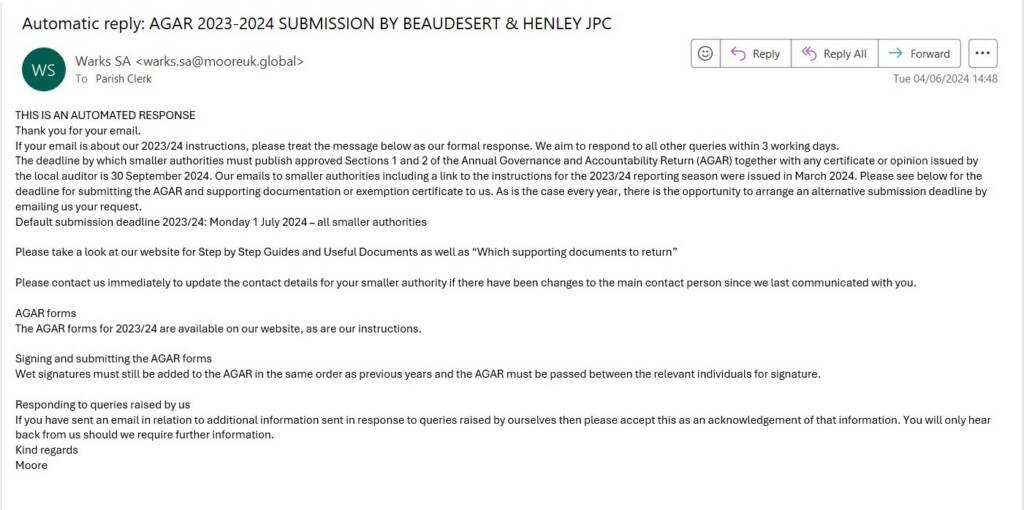

Moore Acknowledgement of Receipt 04.06.2024

Ray Evans – Clerk to the JPC

YEAR 2022-2023

On the 15th of May 2023, the newly elected JPC held their Annual General Meeting.

The matter of the Annual Governance & Accountability Return was considered, see Minute M13, a Governance Statement and, Minute M14. an Accounting Statement on this website. These were duly considered and approved by full Council. However, as the newly elected members may not be familiar with the detail of the return and why it is required, the Chair asked for a meeting with all members to highlight the major aspects of the return. As soon as the outcome of this meeting is clear, the return will be forwarded by post and emailed to the External Auditor in compliance with their instructions, see –

1-2022-23-detailed-instructions

ANNUAL ACCOUNTING STATEMENT-AGAR_2022-23

ANNUAL ACCOUNTING STATEMENT-AGAR_2022-23 [V2]

ANNUAL-GOVERNANCE-STATEMENT-AGAR-22-23

ANNUAL INTERNAL AUDIT REPORT 2022-23

ANNUAL INTERNAL AUDIT REPORT 2022-23[V2]

20-Bank-reconciliation-proforma 22-23

21-Explanation-of-Variances-2022-23 (1)

22-Reconciliation-between-Box-7-and-Box-8-proforma

PERIOD FOR PUBLIC RIGHTS TO BE EXERCISED_2023

covering letter AGAR-littlejohn 03.05.2023

Section 3 – External Auditor Report and Certificate 2022- 23 INTERIM_1396090

AUDIT CLOSURE DOCUMENTS 2022-2023

Covering Letter to Clerk_1398699

Beaudesert & Henley in Arden Joint PC Signed EA 2023_1398709

SA-Notice-of-Conclusion-of-Audit-2023

SECTION 3 EXTERNAL AUDITOR REPORT

Ray Evans

Parish Clerk/RFO to the Beaudesert & Henley in Arden JPC

YEAR 2021-2022

ANNUAL ACCOUNTING STATEMENT 2021-2022

ANNUAL GOVERNANCE STATEMENT 2021-2022

EXPLANATION ON VARIANCES STATEMENT_2021-2022

COVERING LETTER – PKF LITTLEJOHN MAY 22

INTERNAL AUDITORS REPORT 2021-2022

CLOSURE LETTER SEPTEMBER 2022_

PKF CERTIFICATE & INVOICE SEPTEMBER 2022

The JPC has completed and received closure of the 21/22 return. Their opinions and guidance for 22/23 are:

Except for the matters reported below, on the basis of our review of Sections 1 and 2 of the Annual Governance and Accountability Return (AGAR),

in our opinion, the information in Sections 1 and 2 of the AGAR is in accordance with Proper Practices and no other matters have come to our

attention giving cause for concern that relevant legislation and regulatory requirements have not been met.

Section 1, Assertion 3 has been incorrectly completed. In the completion of the Annual Internal Audit Report, the internal auditor has drawn

attention to instances of non-compliance with laws and regulations in respect of Notices of meetings and payroll-related matters. Therefore, the

smaller authority should have responded ‘No’ to this assertion. We understand that both issues have been rectified since the year-end.

The AGAR was not accurately completed before submission for review. Please ensure that amendments are corrected in the prior year

comparatives when completing next year’s AGAR:

The figures in Section 2 Boxes 1 and 8 for the prior year are incorrect due to transcription errors and should read £61,923 and £67,716

respectively.

Section 2, Box 4 for the current year incorrectly includes £187 of items that are not staff costs as defined in the Joint Panel on

Accountability and Governance Practitioners’ Guide. Additionally, Box 6 for the current year includes £6,442 of staff-related costs

which should have been included in the Box 4 figure. The figures in Section 2, Boxes 4 and 6 for the current year should read £26,081

and £82,010 (respectively). Similarly, £1,514 of expenses have incorrectly been included in Box 6 in the prior year, therefore Box 6 in

the comparative column should read £110,608 and Box 4 should read £6,864

PKF fees for providing the external audit report 2021/2022 amounts to £400.00 plus VAT [standard charge] their invoice will be presented for payment at the JPC meeting on the 3rd of October 2022.

YEAR 2020-2021

Please find all pertinent documents for the 20-21 return in the following:

D3 – bank-reconciliation-proforma

D4-explanation-of-variances-proforma

D5 -reconciliation-between-Box-7-and-Box-8-proforma

D7 – provision-for-the-exercise-of-public-rights

Additional IA notes to Beaudesert

ANNUAL GOVERNANCE & ACCOUNTABILITY RETURN [AGAR]

YEAR 2019-2020